After the 2015 auto insurance new deal, how to buy insurance insurance appropriate

Auto insurance and auto insurance reform seems to be closely related to us, but because of the trouble to buy auto insurance; Every year only when the premium is renewed, we will contact the insurance broker; And only out of danger or not out of danger for a year, we will think of premium is really reasonable; The above factors let us to car insurance and car insurance reform will not give too much attention, in two words is numbness�� We are numb to auto insurance, numb to unreasonable terms, numb to unfair payment and premium��

In view of the subject of the problem - " after the new deal of auto insurance, auto insurance insurance should be how to buy appropriate", I have to explain the policy of auto insurance reform�� Today June 1, in the six pilot areas of the country ( Heilongjiang, Guangxi, Shaanxi, Shandong, Chongqing, Qingdao ) implemented Market - oriented reform of commercial auto insurance�� In auto insurance, the owner must buy insurance: compulsory insurance ( 6 under 950 yuan / year, 6 above 1100 yuan / year ) and third party liability insurance ( hereinafter referred to as the three liability insurance )�� The three liability insurance is the most important in the market-oriented reform of commercial auto insurance��

Why do you say that?�� Because there are so many unfair and unreasonable places in previous commercial risks��

I'll take three liability insurance as an example�� Ordinary family car ( less than 6 ) insured three liability insurance of five hundred thousand, a fixed fee of 1721 yuan, and then multiplied by the discount rate of the insurance company to calculate�� The factors affecting the three liability insurance include different insurance companies and different insurance channels�� That is to say, you buy a BMW pay three liability insurance may be the same as a QQ ( in the same insurance company, the same channel )������

Therefore, in the case of more than 10 years of car insurance reform, the commercial insurance reform is the first step to truly break the original unfair auto insurance��

So after the introduction of the new policy, what is the biggest impact on car owners��

My answer is Bring justice��

Before and after the reform, it doesn't affect the choice of what to buy. instead, you need to focus 80 % of your attention on your driving behavior and the remaining 20 % on the model you choose to buy��

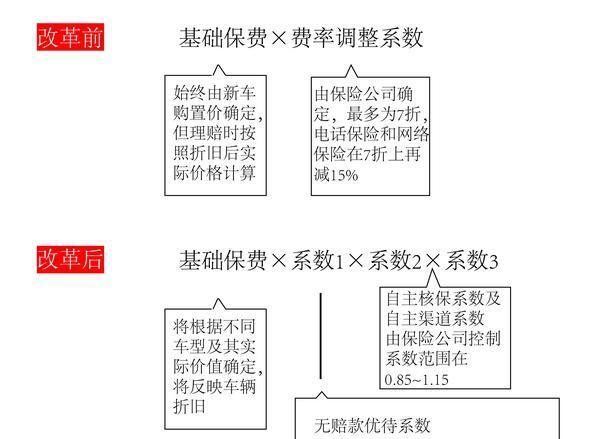

Below I will be on a new and old commercial insurance premium calculation method comparison diagram ~

Left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left

It can be seen from the above that the reformed commercial risks will be more humane��

In particular, the reformed commercial risk calculation factor 1, with the following detailed provisions:

According to the insurance situation of each vehicle in the past three years: no compensation for three consecutive years is 0. 6. No 0 for two consecutive years. 7. Last year was not 0. 8. New insurance or a previous year for 1; Two claim occurred in that previou year were 1. 25. Three times in the previous year was 1. 5. Four times in the previous year were 1. 75. Five times last year and up to 2��

So commercial auto insurance reform will bring about a huge change in premium - your driving behavior security will greatly affect your premium��

After the reform of the basic premium is based on the depreciation rate of the model to change�� German and Japanese car, for example, are relatively protected, and their premium will be relatively higher than other u. S. and Korean cars ( at that same price, with the same age )��

To sum up, individuals think that the reform before and after the purchase of insurance change is not big, some additional risks just buy a peace of mind�� And if your driving habits are good enough not to risk, then your premium coefficient will be relatively low and the additional risk will be reduced accordingly��

Third party liability insurance

Three liability insurance is the highest frequency of commercial insurance, basic to 99. 99 %�� Third party liability insurance compensation to a third party, not including their families�� But after the new business insurance reform, has been included in the family three liability insurance range, after reversing crashed his dad's leg also don't have to lie, say others drive into your dad������

It says the probability of purchasing three liability insurance is 99. 99 %, that's 0. 01 % why not buy it��

There are two answers, pointing to two categories of people�� The first category is a car does not open, even if open only in their own zhuangyuan open, absolutely won't appear a third party�� Even if there is a third party, killed can also be buried directly in the home zhuangyuan buried������ The second kind is the so-called keyboard great god, drive by mouth without legs, home car didn't car is not necessarily������

Then why say three liability insurance, because hit people really expensive very expensive; If you kill people, Emma, you still see it yourself������

The calculation formula prescribed by the state is as follows:

People killed or injured are according to the account to distinguish, divided into urban accounts and rural accounts, urban accounts, of course, will be much more expensive than rural accounts������

Take Shanghai as an example, the city per capita disposable income of 47710 yuan / year�� If you pretend to die a person under the age of 60, you have to compensate TM $ 954200 ( 47710 * 20 ), Nearly a million��������

Even in Shanghai farmers dad, rural per capita disposable income of 21192 yuan / year, die, also have to compensate 423840 yuan ( 21192 * 20 )

These haven't add what mental damage compensation, dependent living expenses������

Even if not killed, seriously disabled you also can't afford to pay����

According to the Shanghai city account:

Level 1 disability, that is, killed, compensate 100 % - 954200 yuan

Secondary disability, compensate 90 % - 8578780 yuan

Level 3 disability, compensate 80 % - 763,360 yuan

������

Ten disabled, compensate 10 % - 95420 yuan

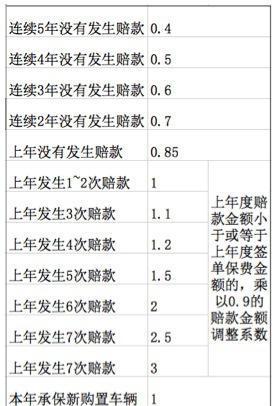

Multi - insurance preferential coefficient: after the three risks and any other insurance are insured ( including the three risks are not exempt from compensation ), you can enjoy this discount�� This offer is automatically given by the insurance company platform, if you meet the conditions, such as insurance + non - compensable, you can enjoy 0. 9 % discount��

2, no compensation preferential coefficient; This refers to a few consecutive years without risk, the coefficient of change please refer to the table below:

Scenario 1: comprehensive portfolio

Insurance portfolio: Traffic insurance, commercial three liability insurance ( 1 million ), car damage insurance, car personnel liability insurance, theft and rescue, glass broken alone, excluding the risk of non-compensation and body scratch loss��

Suggested population Mainly applicable to new drivers of new cars, need comprehensive protection��

Option 2: mass portfolio

Insurance portfolio Compulsory traffic insurance, commercial three liability insurance ( 500,000 ), vehicle damage insurance, vehicle personnel liability insurance, illegal rescue and non - compensation��

Suggested population Suitable for most owners, the vehicle has a fixed parking lot, the owner's driving experience is relatively rich��

Option 3: economic mix

Insurance portfolio Compulsory insurance, commercial three liability insurance ( 300,000 ), car damage insurance and non - deductible��

Suggested population Vehicle owners who have long service life, rich driving experience and are willing to take part of the risks themselves��

Scenario 4: risk portfolio

Insurance portfolio Compulsory insurance

Suggested population : none�� Car owners can't just buy compulsory insurance��

Reason: only the third party in the accident ( that is, the injured party ) is paid for the compulsory insurance, the maximum compensation for casualties is RMB 110,000.00 yuan, hospitalization is RMB 10,000.00 yuan, property loss is RMB 2,000.00 yuan, and the vehicle loss or theft shall be borne by oneself�� Therefore, the risk of the auto insurance scheme is very big, driving on the road, basically belong to the " naked rush" state��

It can be understood that if it is a new car, usually the first year of the car insurance will be in accordance with the comprehensive combination of purchase, but after a year of vehicle running-in and driving experience, auto insurance expires to renew, auto insurance how to buy the most cost - effective��

Planning jun also gives a few combination scheme, the owner might as well be seated:

Option 1: old driver + new car

Reason Because of the rich driving experience of the old driver and good command of the road conditions, the lower amount of third party liability insurance and the lower amount of vehicle personnel liability insurance can be selected, the new car is in good condition, and the self-combustion insurance does not need to be selected; Theft rescue and body scratch risk can be selectively added according to the surrounding parking situation��

Insurance portfolio Commercial three liability insurance ( 300,000 or 500,000 ) + vehicle damage insurance + vehicle personnel liability insurance ( driver + passenger ) + non - compensable

Option 2: old driver + old car

Reason : experienced in driving, you can choose a lower amount of third party liability insurance, but due to the long mileage of the vehicle, such as more than 100,000 kilometers, the car's equipment is old and the probability of spontaneous combustion increases, so you should consider to supplement the self-combustion insurance��

Insurance portfolio Commercial three liability insurance ( 300,000 or 500,000 yuan ) + vehicle damage insurance + vehicle personnel liability insurance ( driver + passenger ) + non - compensation + self - combustion insurance

Option 3: new driver + new car

Reason Driving skills are relatively unfamiliar, the road may bring risks to themselves or the surrounding vehicles, should choose a higher third party liability insurance, vehicle personnel liability insurance should also be fully protected�� Since the vehicle is relatively new, the self-insurance policy may not be selected�� The body scratch risk includes the risk of broken glass alone, can according to the safety of parking place and driving situation, appropriate choice��

Insurance portfolio Commercial three liability insurance ( 500,000 or 1,000,000 ) + vehicle damage insurance + vehicle personnel liability insurance ( driver + passenger ) + theft rescue + body scratch insurance + non - compensable

Option 4: new driver + old car

Reason New driving skills, coupled with the old vehicle, novice wear on the vehicle during the wear and tear will be more, you can consider additional self-combustion risk and glass breakage risk alone��

Insurance portfolio Commercial three liability insurance ( 500,000 or 1,000,000 ) + vehicle damage insurance + vehicle personnel liability insurance ( driver + passenger ) + self-combustion insurance + glass breakage insurance + non - compensable

Final summary:

1, compulsory insurance must be on;

2, car damage insurance is to compensate their own car, must be on;

3, third party liability insurance must be on, the recommended amount of 50 million or 1 million, not bad money on more;

4, the car personnel liability insurance to, but don't have to be too much, the driver and passengers per person to protect 10 thousand, the premise is that there is already a personal accident insurance�� If there is no accident insurance, it is better to buy a accident insurance directly, about 100 to 200 yuan a year, the scope of protection not only package ordinary accident, and the accident caused by the train, subway, driving and other accidents;

5, vehicle scratch risk and glass breakage risk is expensive, and security content with car damage risk overlap, so you can not buy; 6, car mileage is more, the purchase year is long, the best buy a self-combustion insurance, new car can not buy;

7, regardless of the free price is cheap, and can maximize avoid economic risk, suggested to buy;

Remind each owner, if received a phone call from the auto insurance sales personnel, might as well let the other party to calculate the total cost of this year's renewal, have don't understand more ask, don't because the other party to give rebates or gifts of auto supplies, such as CarLog, car maintenance and so on is easily insured, we are to buy insurance, not buy gifts�� More than their price, see which risks must be cast, which can not cast, spend the least money to buy the right insurance��

Even at the previous rate of 100,200 is not cost - effective�� Scratch coverage is still relatively small because the leverage ratio is too low�� Give a modified insurance combination: car damage, 300,000 or 1,000,000, seat insurance 1 + 4, glass insurance�� This is the basic combination�� Glass insurance is to protect a premium is not high, 20 people now hit a car glass is a bit more, glass broken car damage alone is not compensate��

Auto insurance and auto insurance reform seems to be closely related to us, but because of the trouble to buy auto insurance; Every year only when the premium is renewed, we will contact the insurance broker; And only out of danger or not out of danger for a year, we will think of premium is really reasonable; The above factors let us to car insurance and car insurance reform will not give too much attention, in two words is numbness。 We are numb to auto insurance, numb to unreasonable terms, numb to unfair payment and premium。

In view of the subject of the problem - " after the new deal of auto insurance, auto insurance insurance should be how to buy appropriate", I have to explain the policy of auto insurance reform。 Today June 1, in the six pilot areas of the country ( Heilongjiang, Guangxi, Shaanxi, Shandong, Chongqing, Qingdao ) implementedMarket - oriented reform of commercial auto insurance。 In auto insurance, the owner must buy insurance: compulsory insurance ( 6 under 950 yuan / year, 6 above 1100 yuan / year ) and third party liability insurance ( hereinafter referred to as the three liability insurance )。 The three liability insurance is the most important in the market-oriented reform of commercial auto insurance。

Why do you say that?? Because there are so many unfair and unreasonable places in previous commercial risks!

I'll take three liability insurance as an example。 Ordinary family car ( less than 6 ) insured three liability insurance of five hundred thousand, a fixed fee of 1721 yuan, and then multiplied by the discount rate of the insurance company to calculate。 The factors affecting the three liability insurance include different insurance companies and different insurance channels。 That is to say, you buy a BMW pay three liability insurance may be the same as a QQ ( in the same insurance company, the same channel )。。。

Therefore, in the case of more than 10 years of car insurance reform, the commercial insurance reform is the first step to truly break the original unfair auto insurance。

So after the introduction of the new policy, what is the biggest impact on car owners?

My answer is Bring justice。

Before and after the reform, it doesn't affect the choice of what to buy. instead, you need to focus 80 % of your attention on your driving behavior and the remaining 20 % on the model you choose to buy。

Below I will be on a new and old commercial insurance premium calculation method comparison diagram ~

Left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left left

It can be seen from the above that the reformed commercial risks will be more humane。

In particular, the reformed commercial risk calculation factor 1, with the following detailed provisions:

According to the insurance situation of each vehicle in the past three years: no compensation for three consecutive years is 0. 6. No 0 for two consecutive years. 7. Last year was not 0. 8. New insurance or a previous year for 1; Two claim occurred in that previou year were 1. 25. Three times in the previous year was 1. 5. Four times in the previous year were 1. 75. Five times last year and up to 2。

So commercial auto insurance reform will bring about a huge change in premium - your driving behavior security will greatly affect your premium。

After the reform of the basic premium is based on the depreciation rate of the model to change。 German and Japanese car, for example, are relatively protected, and their premium will be relatively higher than other u. S. and Korean cars ( at that same price, with the same age )。

To sum up, individuals think that the reform before and after the purchase of insurance change is not big, some additional risks just buy a peace of mind。 And if your driving habits are good enough not to risk, then your premium coefficient will be relatively low and the additional risk will be reduced accordingly。

Third party liability insurance

Three liability insurance is the highest frequency of commercial insurance, basic to 99. 99 %。 Third party liability insurance compensation to a third party, not including their families。 But after the new business insurance reform, has been included in the family three liability insurance range, after reversing crashed his dad's leg also don't have to lie, say others drive into your dad。。。

It says the probability of purchasing three liability insurance is 99. 99 %, that's 0. 01 % why not buy it?

There are two answers, pointing to two categories of people。 The first category is a car does not open, even if open only in their own zhuangyuan open, absolutely won't appear a third party。 Even if there is a third party, killed can also be buried directly in the home zhuangyuan buried。。。 The second kind is the so-called keyboard great god, drive by mouth without legs, home car didn't car is not necessarily。。。

Then why say three liability insurance, because hit people really expensive very expensive; If you kill people, Emma, you still see it yourself。。。

The calculation formula prescribed by the state is as follows:

People killed or injured are according to the account to distinguish, divided into urban accounts and rural accounts, urban accounts, of course, will be much more expensive than rural accounts。。。

Take Shanghai as an example, the city per capita disposable income of 47710 yuan / year。 If you pretend to die a person under the age of 60, you have to compensate TM $ 954200 ( 47710 * 20 ), Nearly a million!!!!

Even in Shanghai farmers dad, rural per capita disposable income of 21192 yuan / year, die, also have to compensate 423840 yuan ( 21192 * 20 )

These haven't add what mental damage compensation, dependent living expenses。。。

Even if not killed, seriously disabled you also can't afford to pay。。

According to the Shanghai city account:

Level 1 disability, that is, killed, compensate 100 % - 954200 yuan

Secondary disability, compensate 90 % - 8578780 yuan

Level 3 disability, compensate 80 % - 763,360 yuan

。。。

Ten disabled, compensate 10 % - 95420 yuan

Multi - insurance preferential coefficient: after the three risks and any other insurance are insured ( including the three risks are not exempt from compensation ), you can enjoy this discount。 This offer is automatically given by the insurance company platform, if you meet the conditions, such as insurance + non - compensable, you can enjoy 0. 9 % discount。

2, no compensation preferential coefficient; This refers to a few consecutive years without risk, the coefficient of change please refer to the table below:

Scenario 1: comprehensive portfolio

Insurance portfolio: Traffic insurance, commercial three liability insurance ( 1 million ), car damage insurance, car personnel liability insurance, theft and rescue, glass broken alone, excluding the risk of non-compensation and body scratch loss。

Suggested population Mainly applicable to new drivers of new cars, need comprehensive protection。

Option 2: mass portfolio

Insurance portfolio Compulsory traffic insurance, commercial three liability insurance ( 500,000 ), vehicle damage insurance, vehicle personnel liability insurance, illegal rescue and non - compensation。

Suggested population Suitable for most owners, the vehicle has a fixed parking lot, the owner's driving experience is relatively rich。

Option 3: economic mix

Insurance portfolio Compulsory insurance, commercial three liability insurance ( 300,000 ), car damage insurance and non - deductible。

Suggested population Vehicle owners who have long service life, rich driving experience and are willing to take part of the risks themselves。

Scenario 4: risk portfolio

Insurance portfolio Compulsory insurance

Suggested population : none。 Car owners can't just buy compulsory insurance。

Reason: only the third party in the accident ( that is, the injured party ) is paid for the compulsory insurance, the maximum compensation for casualties is RMB 110,000.00 yuan, hospitalization is RMB 10,000.00 yuan, property loss is RMB 2,000.00 yuan, and the vehicle loss or theft shall be borne by oneself。 Therefore, the risk of the auto insurance scheme is very big, driving on the road, basically belong to the " naked rush" state。

It can be understood that if it is a new car, usually the first year of the car insurance will be in accordance with the comprehensive combination of purchase, but after a year of vehicle running-in and driving experience, auto insurance expires to renew, auto insurance how to buy the most cost - effective?

Planning jun also gives a few combination scheme, the owner might as well be seated:

Option 1: old driver + new car

Reason Because of the rich driving experience of the old driver and good command of the road conditions, the lower amount of third party liability insurance and the lower amount of vehicle personnel liability insurance can be selected, the new car is in good condition, and the self-combustion insurance does not need to be selected; Theft rescue and body scratch risk can be selectively added according to the surrounding parking situation。

Insurance portfolio Commercial three liability insurance ( 300,000 or 500,000 ) + vehicle damage insurance + vehicle personnel liability insurance ( driver + passenger ) + non - compensable

Option 2: old driver + old car

Reason : experienced in driving, you can choose a lower amount of third party liability insurance, but due to the long mileage of the vehicle, such as more than 100,000 kilometers, the car's equipment is old and the probability of spontaneous combustion increases, so you should consider to supplement the self-combustion insurance。

Insurance portfolio Commercial three liability insurance ( 300,000 or 500,000 yuan ) + vehicle damage insurance + vehicle personnel liability insurance ( driver + passenger ) + non - compensation + self - combustion insurance

Option 3: new driver + new car

Reason Driving skills are relatively unfamiliar, the road may bring risks to themselves or the surrounding vehicles, should choose a higher third party liability insurance, vehicle personnel liability insurance should also be fully protected。 Since the vehicle is relatively new, the self-insurance policy may not be selected。 The body scratch risk includes the risk of broken glass alone, can according to the safety of parking place and driving situation, appropriate choice。

Insurance portfolio Commercial three liability insurance ( 500,000 or 1,000,000 ) + vehicle damage insurance + vehicle personnel liability insurance ( driver + passenger ) + theft rescue + body scratch insurance + non - compensable

Option 4: new driver + old car

Reason New driving skills, coupled with the old vehicle, novice wear on the vehicle during the wear and tear will be more, you can consider additional self-combustion risk and glass breakage risk alone。

Insurance portfolio Commercial three liability insurance ( 500,000 or 1,000,000 ) + vehicle damage insurance + vehicle personnel liability insurance ( driver + passenger ) + self-combustion insurance + glass breakage insurance + non - compensable

Final summary:

1, compulsory insurance must be on;

2, car damage insurance is to compensate their own car, must be on;

3, third party liability insurance must be on, the recommended amount of 50 million or 1 million, not bad money on more;

4, the car personnel liability insurance to, but don't have to be too much, the driver and passengers per person to protect 10 thousand, the premise is that there is already a personal accident insurance。 If there is no accident insurance, it is better to buy a accident insurance directly, about 100 to 200 yuan a year, the scope of protection not only package ordinary accident, and the accident caused by the train, subway, driving and other accidents;

5, vehicle scratch risk and glass breakage risk is expensive, and security content with car damage risk overlap, so you can not buy; 6, car mileage is more, the purchase year is long, the best buy a self-combustion insurance, new car can not buy;

7, regardless of the free price is cheap, and can maximize avoid economic risk, suggested to buy;

Remind each owner, if received a phone call from the auto insurance sales personnel, might as well let the other party to calculate the total cost of this year's renewal, have don't understand more ask, don't because the other party to give rebates or gifts of auto supplies, such as CarLog, car maintenance and so on is easily insured, we are to buy insurance, not buy gifts。 More than their price, see which risks must be cast, which can not cast, spend the least money to buy the right insurance。

Even at the previous rate of 100,200 is not cost - effective。 Scratch coverage is still relatively small because the leverage ratio is too low。 Give a modified insurance combination: car damage, 300,000 or 1,000,000, seat insurance 1 + 4, glass insurance。 This is the basic combination。 Glass insurance is to protect a premium is not high, 20 people now hit a car glass is a bit more, glass broken car damage alone is not compensate。

Comments

Post a Comment